2024 Is Shaping up to Be a Difficult Year for the Watch Industry

Swiss Watch Export Data Provided by FHS and Richemont's Financial Statement, show some signs of decline for Q1 2024

2023 was another record year for the watch industry, exports hit a new record, growing 7.6% over 2022, reaching a combined total of CHF 26.7 billion.

The result achieved was truly significant and is a fitting reward for putting watches back on the crest of the wave, an object that so many believed was now an accessory with a useless function surpassed by new technologies.

Contrary to everyone (or almost everyone) in recent years, timepieces have experienced unexpected growth, an enthusiasm that has overwhelmed everyone in the market, from the resellers who have benefited from a secondary market that seemed to show no signs of stopping to the brands themselves, which have often had to contend with a demand for product that was higher than the supply they could provide. On the one hand, however, the secondary market began to show signs of decline as early as mid-2022, while the primary market, i.e., the one where the maisons operate, has remained very stable with consistently excellent results as evidenced by the Swiss watch export figures that have always been on the rise in recent years, up to a record 2023.

Swiss Wristwatch Exports Enjoy Another Record Year in 2023

Stay ahead of the curve – subscribe to our weekly blog to keep up with the latest news, info and insights from the watch market

However, growth cannot last forever, and early figures for 2024 are beginning to portend a 2024 that may be less bright than previous years. In fact, already the second half of 2023 had already given an indication of this, in fact the first six months were the best with an increase of even +11.8%, offset by the second half of the year that saw a slowdown in growth, stopping at only +3.6%.

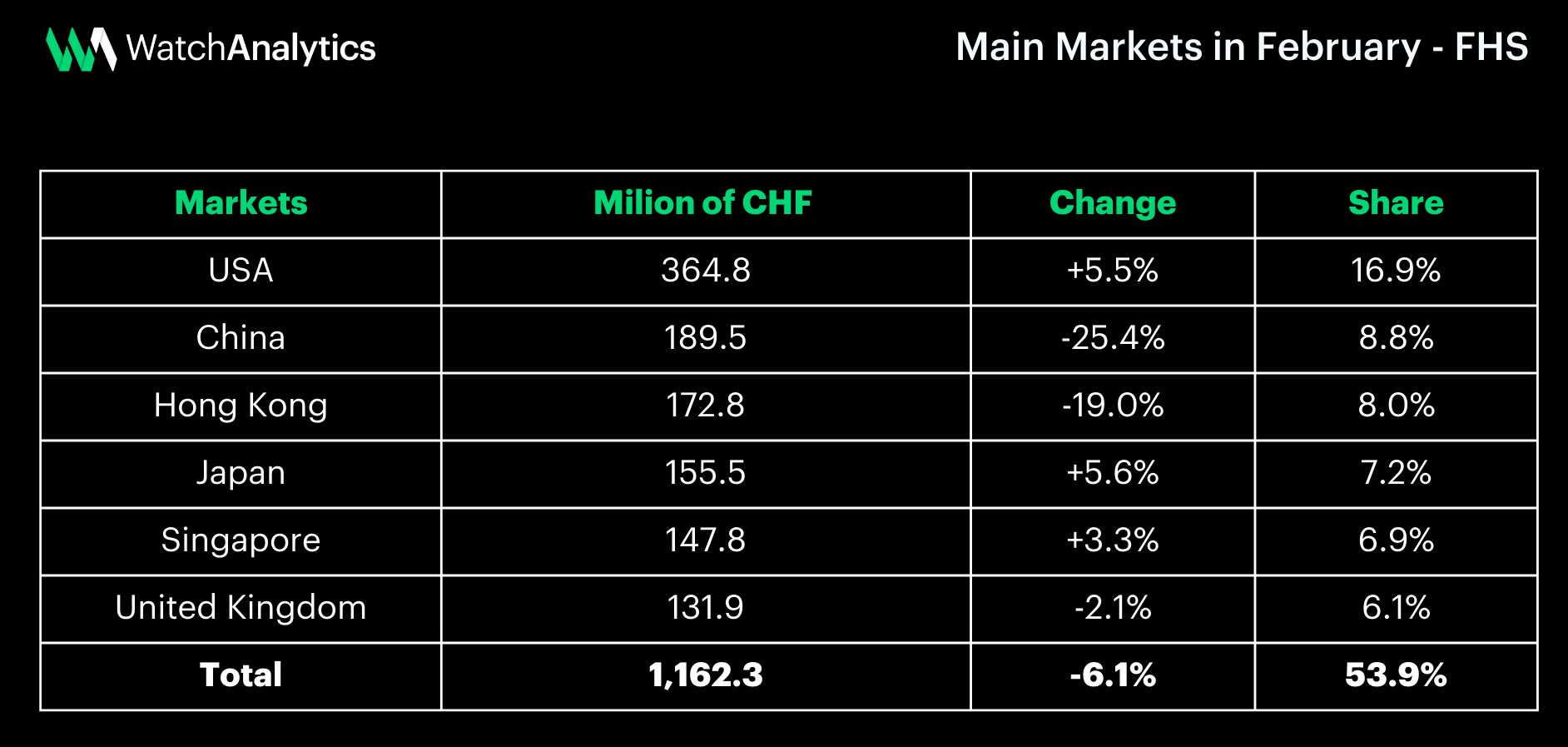

The early signs of late 2023, became more and more pronounced this year, in February exports recorded a first significant decline of -3.8%. On the one hand, some markets continued to grow: the United States +5.5%, Japan (+5.6%), Singapore (+3.3%), and the United Arab Emirates (+8.9 percent), but not enough to offset the sharp decline in China (-25.4%) and Hong Kong (-19.0%) and a slight drop in Europe of -3.5%.

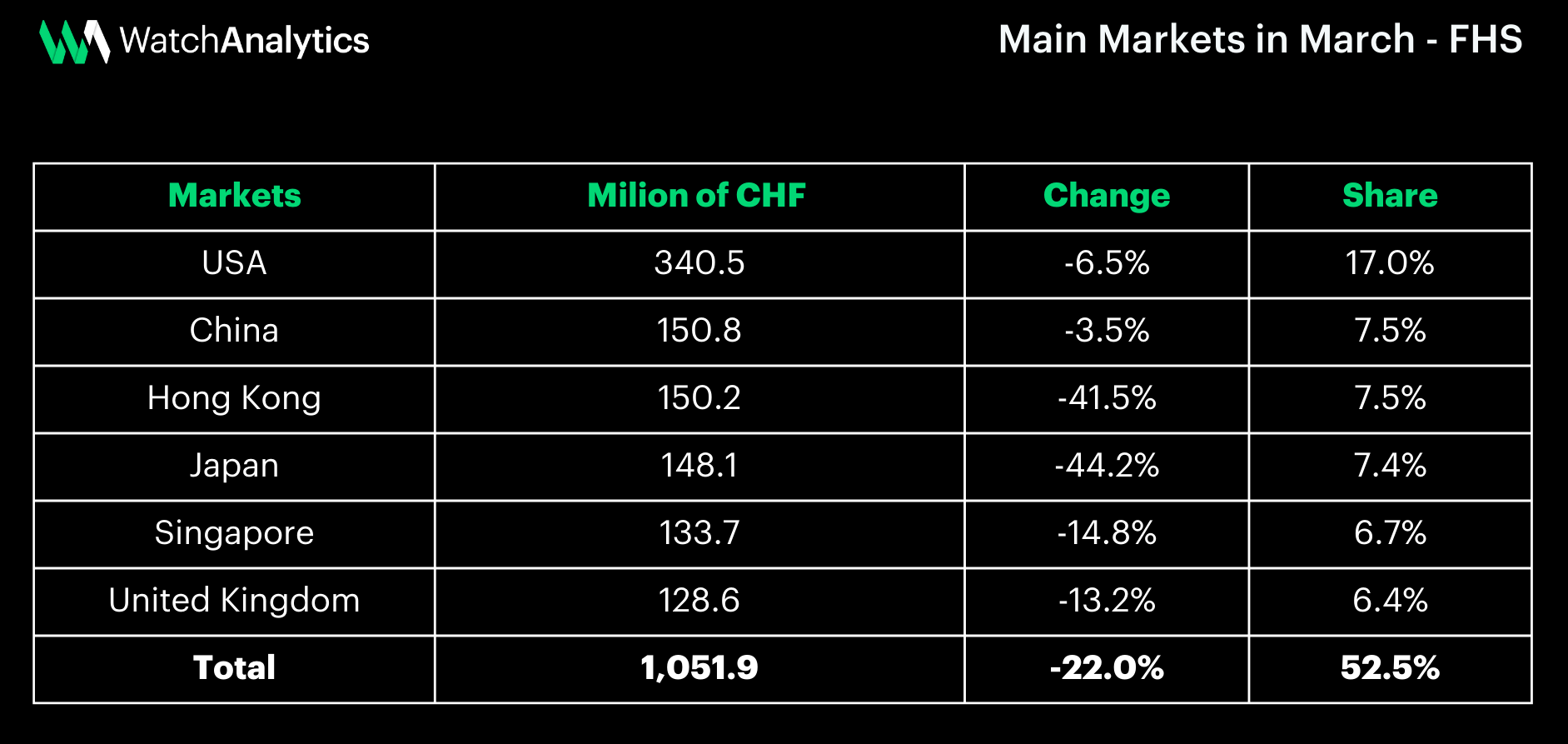

In March, the export figure fell even further, with exports plummeting by -16.1% (compared to March 2023).

If the previous month some countries had recorded positive performance, this time exports highlighted negative data worldwide. Even the United States (-6.5%), Japan (-3.5%) and the United Arab Emirates (-3.6%), which had been growing in February, have to surrender to a significant drop this time, although they remain less affected than other countries. The steepest drop is seen in China, which suffers -41.5%, falling to a lower level than in March 2020, when, as FHS points out, the sector came to a virtual standstill in the middle of the month due to the Covid pandemic. Hong Kong experienced a similar change, dropping -44.2%, while Singapore (-14.8%).

The slump in exports especially related to China and Asian countries is a factor that is beginning to cause some concern, especially since these are the markets that have grown the most in the past few years and are also behind the big boom period seen between 2020 and 2023.

In addition to the export figure provided each month by the Federation of the Swiss Watch Industry, confirmation of a difficult start to 2024 for Asia also comes to us from the financial statements of Richemont, the company that owns Cartier, A. Lange & Söhne, IWC, Jaeger Le Coultre and many other luxury brands.

The Swiss group, unlike Swatch Group and LVMH which use December 31 as a benchmark, closes its fiscal year on March 31 and therefore is able to give an adequate disclosure of how business was in the first 3 months of the new year.

In conjunction with the release of the report, Richemont announced that Nicolas Bos, currently CEO of Van Cleef & Arpels, will become the new CEO, effective June 1, 2024.

The company performed very well, with sales increasing by 3% at current exchange rates and 8% at constant exchange rates, and overall sales grew by 7% to €20.6 billion versus €19.9 billion in 2023.

The positive performance is mainly due to the jewelry department, which made the bulk of sales, coming in at €14.2 billion, up 6% at current rates and 12% at constant rates. Watches, on the other hand, fared a bit worse, growing only +3% at current rates and 2% at constant rates, coming in at a total result of €3.8 billion.

In particular, says Richemont, iconic collections have shown remarkable resilience, including Lange 1 for A. Lange & Söhne, Portugieser for IWC, Reverso for Jaeger-LeCoultre, Luminor for Panerai, Polo for Piaget, and Traditionnelle for Vacheron Constantin.

Going to look at the overall data for the quarters of the year, however, again there is a major decline in Asia Pacific during Q4. From April to June 2023, this geographic area registered a +40% increase over Q1 2022, a much lower percentage in Q2 (+8%), a strong recovery at the end of the year (October-December) +13% and then registering a -12% decline in the period between January and March 2024.

The slowdown in China is thus confirmed not only by the data proposed by FHS but also by Richemont's financial statement.

Certainly the tremendous growth of the past few years in this geographic area is now finding a period of stabilization; it will now be interesting to see whether this is a moment of fomenting market uncertainty, or will it be a trend that will continue for the rest of the year.