Swatch Group: Another Victim of the Chinese Market Collapse

Swatch Group struggles as China's luxury market falters, uncover the highs and lows of their performance in the first half of 2024

A few days ago, Swatch Group released its half-year financial report as of June 30, 2024, confirming trends we had begun to highlight in previous articles, particularly when analyzing competitor Richemont's financial situation.

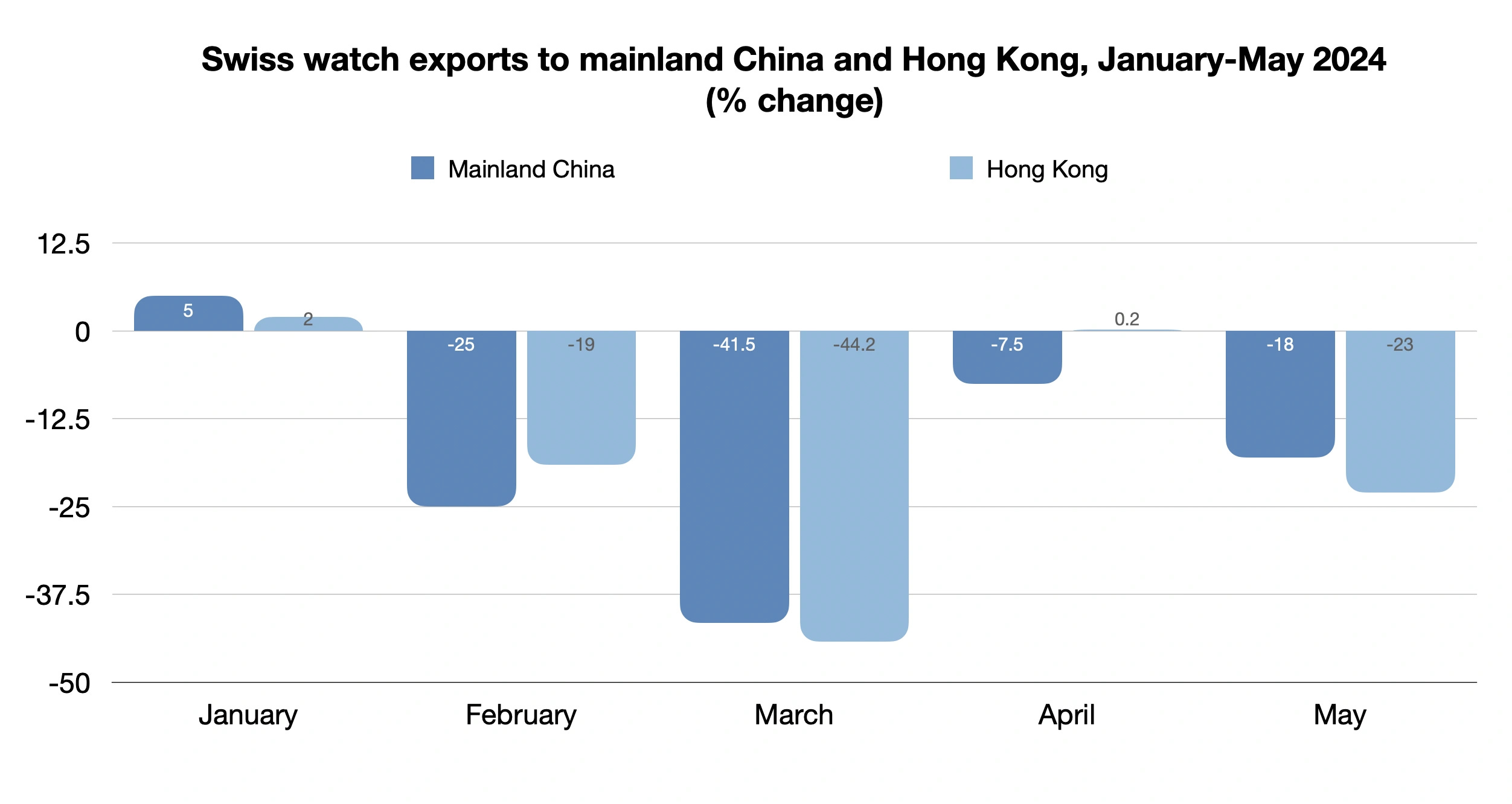

While the secondary market began showing signs of decline in mid-2022, the primary market remained stable with excellent results, as evidenced by steadily increasing Swiss watch exports, culminating in a record year in 2023. However, this growth could not last forever, and early data from 2024 suggest a potential slowdown. Indeed, the second half of 2023 already showed a deceleration, with an increase of 3.6% compared to 11.8% in the first half.

The first signs of trouble in 2024 became evident as early as February, with exports declining by 3.8%. Despite growth in some markets like the United States (+5.5%), Japan (+5.6%), Singapore (+3.3%), and the United Arab Emirates (+8.9%), the sharp decline in China (-25.4%) and Hong Kong (-19.0%) had a significant impact. In March, the situation worsened with exports falling by 16.1% compared to the same month in 2023, with significant declines in all major markets, including the United States, Japan, and the United Arab Emirates.

The negative performance continued in recent months, and overall, in the first six months of 2024, as reported by FHS, exports to China showed a net decline of -21.6%, dragging down Hong Kong (-19.9%) with them.

The drop in exports to China and other Asian countries is particularly concerning since these markets had driven growth between 2020 and 2023. Confirmations of a difficult start to 2024 for Asia also come from the financial results of Richemont, owner of luxury brands such as Cartier and Jaeger LeCoultre. Despite a 7% increase in sales to €20.6 billion in 2023, the watch division posted modest growth of 3%.

Richemont ends its fiscal year on March 31 of each year, so the financial report a few months ago was the first signal of what is starting to happen this year to the watch industry. The data show a sharp decline in the Asia-Pacific region in the last quarter of the fiscal year, with a 12% decrease between January and March 2024. This trend confirms the FHS data and suggests that the extraordinary growth of recent years is now entering a period of stabilization.

H1 2024 Performance of Swatch Group

Swatch Group's half-year results only confirm the early warning signs that emerged.

The Group reported a net sales decline of -14.3% at current exchange rates (-10.7% constant exchange rates) compared to the previous year, stopping at CHF 3,445 million.

As explained in the Swatch Group report, the decline in sales and profits was mainly attributed to the drastic reduction in demand for luxury goods in China, including Hong Kong and Macau, and in Southeast Asian markets heavily dependent on Chinese tourists. This had a significant impact on the results due to the strong presence of the Group's brands in the region. However, contrary to this negative trend, the Swatch brand recorded a 10% increase in sales in China compared to the previous year, thanks to the great success of the Moonswatch.

Wholesale sales in Europe fell by over 10%, influenced by retailers' concerns about excessive stock levels due to geopolitical conflicts. Additionally, the production sector recorded strongly negative operating results due to the Group's decision to maintain all production capacities and not lay off staff despite the decline in orders from both third parties and its brands.

The Group's operating margin in the watches and jewelry segment (excluding production) fell to 11.0% from 19.0% the previous year, also influenced by the decision to maintain marketing investments.

United States and Japan Drive Retail Sales

Despite the challenging situation, there have been some significant successes. In the United States, sales maintained the record levels of 2023, while in Japan, one of the most important markets for luxury goods and the third-largest export market for Swiss watches, sales increased by over 30% compared to the previous year. Other important markets such as South Korea, India, and the United Arab Emirates also exceeded expectations, with performances better than the previous year.

In Europe, the Group's retail sales remained stable compared to the previous year, despite geopolitical conflicts making many European retailers cautious about restocking. Switzerland and Spain recorded particularly positive performances.

The Group's retail segment exceeded 45% of total sales in the watches and jewelry sector for the first time. This segment saw an increase in sales compared to the previous year in local currencies, excluding China.

What is Happening in China?

According to JingDaily, some analysts link this decline to several economic factors. One of the main causes is the contraction of real estate values in China, which has reduced consumer confidence and, consequently, spending on luxury goods. Additionally, the strength of the Swiss franc has made Swiss watches more expensive and less attractive in some markets.

Another factor impacting demand in China has been Beijing's ongoing crackdown on extravagant displays of wealth. The Chinese government has been promoting more modest behavior, discouraging the purchase of luxury items such as high-end watches, often seen as status symbols. Furthermore, Chinese consumers are increasingly purchasing luxury goods abroad, taking advantage of post-pandemic travel to shop in destinations like Japan and Singapore. This shift may have negatively influenced domestic sales while boosting sales figures in other markets.